Grand illusion: Why Europe should question wisdom of "austerity"

With investors already seeming to lose faith in the latest solution to Europe's debt crisis, the Continent's future -- and of the world economy -- may ride on one country: Latvia.

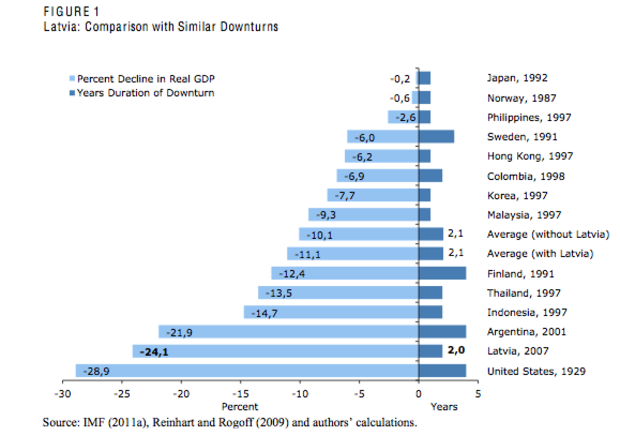

The Baltic nation, whose population of roughly 2.2 million makes it smaller than the borough of Brooklyn in New York City, represents a key test case for the economic polices European officials are counting on to revive the region. In part, that's because the 2008 financial crisis hit Latvia harder than any other country in

the world. In two years, nearly one-quarter of its GDP disappeared

(compared with 29 percent for the U.S. during the Great Depression; see

chart below), forcing it to seek a $10.2 billion bailout from the EU and the IMF. It's also because Latvia, an aspiring member of the eurozone, has spent the last two years implementing the same contractionary fiscal remedies that have been prescribed in Greece, Ireland, Portugal and other troubled European economies.

In short, Latvia is a laboratory. It is effectively a pilot study on whether economic "austerity" -- tax hikes, government spending cuts, wage reductions and other measures to shrink a nation's debt -- works better than the alternative of fiscal and monetary expansion. Austerity supporters believe Latvia's resurgence suggests their preferred strategy works. Says WaPo columnist Robert Samuelson in contrasting Latvia's embrace of austerity with the contentious debate in the U.S. over how to boost the economy:

What distinguished Latvia's experience from our own is that, once people recognized the gravity of the crisis, they came together to support the necessary, if harsh, policies to stop the free-fall and restore stability. The economy is now growing again, and although joblessness remains horrific... it is gradually declining.

The cost of austerity

In some ways, that's undeniably true. Unemployment in Latvia, which shot up from 5.3 percent before the financial crisis in 2007 to more than 20 percent in 2010, has since receded to 14.4 percent. Private demand and corporate investment are up, along with retail sales and industrial production. Growth is robust, reaching 6.6 percent in the third-quarter even as the broader regional economy cools. Financial markets also show renewed faith in Latvia, with the government recently expressing confidence that its borrowing costs are set to fall.

Others aren't convinced by Latvia's comeback. Its policy of "internal devaluation" -- in which countries seek to increase their competitiveness by maintaining a fixed exchange rate, keeping a lid on worker pay and boosting productivity -- has had severe social and economic costs, according to the Center for Economic and Policy Research. Factoring in people who have dropped out of the labor force or who are involuntarily working part-time, Latvia's unemployment rate remains above 21 percent, the Washington think-tank says in a recent report. Count the more than 100,000 Latvians who have gone abroad in search of a job and that figure could be as high as 29 percent. The government's focus on lowering wages and curbing social services also suggests that income inequality is increasing.

More important, it wasn't shifting toward austerity in 2009 that sparked Latvia's economy, according to the CEPR -- it was a rise in inflation. After tumbling in 2009-10, prices and wages have rebounded this year. That helped reduce interest rates, spur lending and cut the country's borrowing costs. Meanwhile, the Latvian government never really did tighten its fiscal policies during the worst of the financial crisis, as austerity advocates claim. The proof -- Latvia's fiscal deficit was the same in 2010 as the previous year. The CEPR notes:

[I]t appears that the recovery resulted from the government not adopting the fiscal tightening for 2010 that was prescribed by the IMF, as well as expansionary monetary policy caused by rising inflation....This has implications for the current debate over crisis in the eurozone, since pro-cyclical policies are being implemented in a number of countries. If Latvia had provided a successful example of recovery through internal devaluation, it might be relevant to the weaker eurozone economies that have locked themselves into pro-cyclical fiscal policies and are to varying degrees relying on the prospect of internal devaluation to eventually boost their economies through net exports. The Latvian case provides further evidence that this can be a very costly strategy and one that does not work.

A better path?

Latvia's recovery-through-austerity also must be contrasted with the experience of countries that pursued the opposite course. Take Argentina. After a calamitous financial crisis culminated in Latin America's third-largest economy defaulting on its debt in 2001, over the next seven years Argentina proceeded to nearly triple its level of government spending. It increased retirement, unemployment, health care and other welfare benefits; boosted funding for various sectors of the economy; and cut subsidies for profitable industries. Argentina also resisted IMF pressure to repay its creditors in full.

The result: Between 2002 and 2011, Argentina's economy grew 94 percent -- the fastest growth rate in the Western Hemisphere over that period. Government revenue rose from 15 percent of GDP in 2002 to more than 23 percent seven years later, while unemployment declined from more than 16 percent to just over 7 percent today. GDP is on track this year to rise 8 percent.

Of course, it's impossible to know how Latvia would've fared if it had rejected austerity and instead turned to fiscal stimulus to re-start its economy. But the country's slower recovery compared with that of Argentina (and other nations, like Iceland, that have sought to grow their way out of a financial crisis) undermines the view that fiscal contraction represents the best path to renewal.

Yet that is the path that Europe's mandarins, notably German Chancellor Angela Merkel and French President Nicolas Sarkozy, are determined to take. Investors seem less certain. If the latter are eventually proved right, Latvia's recovery is likely to be brief, a "false positive" in an economic experiment gone awry.