A new tool for retirees who expect to live long

For many retirees, outliving their retirement income is a worrisome possibility. But what can you do to avoid that undesirable fate? Many financial commentators now advocate that you devote a portion of your retirement income portfolio to deferred lifetime payout annuities that start at an advanced age, such as age 80 or 85.

Known as longevity annuities, they've received a boost from recent U.S. Treasury guidance that defined "qualified longevity annuity contracts" and clarified how they can be paid from IRAs and 401(k) accounts. In the process, the Treasury coined a new acronym -- QLAC.

But before you rush out to buy one, you need to do some homework to figure out if a QLAC is a good idea for your retirement income portfolio. You can gain insights from a recent study by the Stanford Center on Longevity (SCL), in collaboration with the Society of Actuaries (SOA). (I was a co-author of it with Wade Pfau and Joe Tomlinson.)

It turns out that there are a handful of reasonable ways to use a QLAC in your retirement income portfolio, but you need to be clear about your reasons. And it may be that using a QLAC is easier said than done.

One strategy is to use a small portion of your retirement savings, say 15 percent, to buy a QLAC starting at age 85 to cover the possibility that you might live a long time. The QLAC would then pay you for the rest of your life after age 85, no matter how long you live. Until age 85, you'd invest and withdraw from the rest of your savings, using a systematic withdrawal plan (SWP). This would give you control over and access to that portion of your savings, features that usually aren't available with traditional payout annuities.

The SCL/SOA study looked at 36 possible integrated SWP/QLAC strategies and compared them to more conventional retirement income strategies such as stand-alone SWPs, stand-alone annuities and combinations of SWPs and traditional annuities. The projections show that in some cases, it may be possible to boost your expected lifetime retirement income from a SWP/QLAC strategy. The challenge, however, is that these strategies create the potential for a significant disruption in your income between ages 84 and 85.

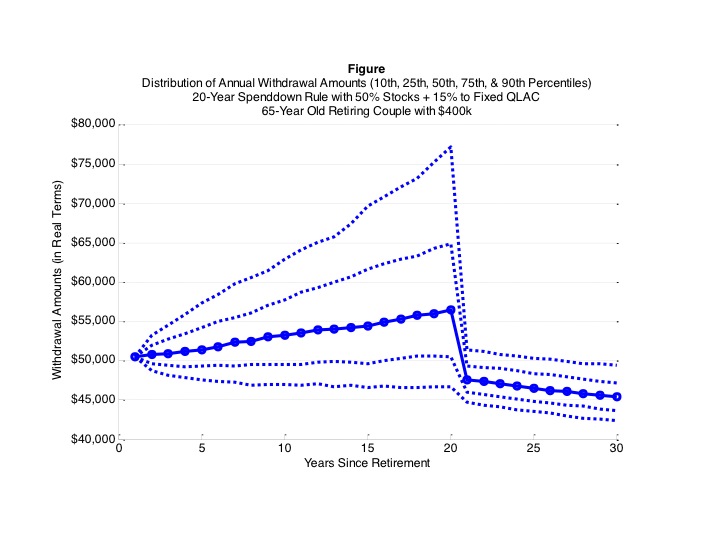

The chart below illustrates this challenge for one particular strategy that devoted 15 percent of assets at age 65, invested remaining assets 50 percent in stocks and withdrew from assets each year in sufficient amounts to exhaust invested assets by age 85. It projects the total annual amount of retirement income at each age between age 65 and 95 including Social Security, income from the SWP until age 85 and income from the QLAC after age 85.

The bold line represents the expected economic scenario, the top lines represent favorable economic scenarios and the bottom lines represent unfavorable scenarios. For this particular strategy, retirement income drops significantly under most scenarios at age 85. The SCL/SOA study shows similar outcomes with other SWP/QLAC strategies.

This doesn't necessarily mean that such strategies are undesirable. One way to respond to this potential is by making adjustments throughout retirement in the withdrawal and investment strategy for the SWP so that the income amounts line up better between ages 84 and 85. This requires either a very informed and capable retiree, or the ongoing attention of a qualified retirement advisor.

Here are the critical decisions that must be made for integrated SWP/QLAC strategies:

- Determine the portion of initial assets devoted to the QLAC.

- Develop a SWP withdrawal and asset allocation approach that minimizes disruptions in the amount of income between ages 84 and 85.

- Decide whether to purchase a QLAC that pays a death benefit before age 85, which produces a lower retirement income compared to no death benefit.

These decisions show why such strategies might be easier said than done (you can try this online calculator to help you work through this challenge).

In addition to the integrated SWP/QLAC strategy, here are other possible uses of QLACs:

- Some retirees might want to define the absolute minimum amount of retirement income they need at an advanced age as a form of insurance against living a long time. They would then work or draw on financial assets until that age and be willing to tolerate the potential disruption in income at the advanced age.

- Buy a QLAC with an earlier starting age, such as 75, and work or deploy minimum required withdrawals from savings until that age, or both.

- Layer additional income from a QLAC starting at age 80 or 85, to help pay for medical or long-term care costs that typically increase at these ages.

QLACs are one of the latest innovations in retirement income planning, but that doesn't mean everybody needs one. Give careful consideration to how they might be used successfully in your retirement income portfolio. If you aren't comfortable making these analyses on your own, find a competent and unbiased financial advisor to help you.