3 dire warnings coming from the bond market

The post-election stock market surge has been getting all the attention. Donald Trump’s surprise victory surprisingly pushed the Dow Jones industrials index to a new record high on hopes of an aggressive fiscal stimulus push from his proposed tax cuts and infrastructure spending.

But other markets have been decidedly less enthusiastic about the flaxen-haired billionaire who has shaken the political establishment. Emerging market currencies have been hammered. Tech stocks have wilted.

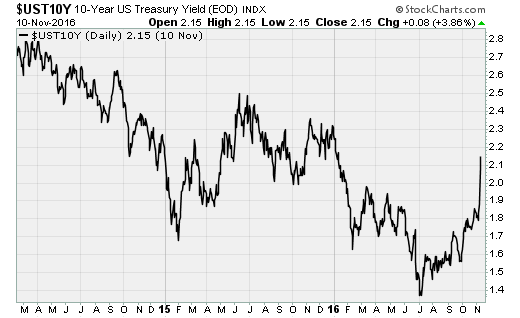

And, arguably most important, bond prices have plummeted, pushing the 10-year Treasury yield to 2.2 percent (yields and prices move in opposite directions). That’s the highest level since January. The iShares 20+ Treasury Bond (TLT) exchange-traded fund has dropped more than 14 percent from its July high, with half of the decline coming this week alone.

Here are three warnings to be taken from the harrowing decline in bond prices:

Inflation is coming

The primary fuel for the surge in interest rates (chart above), and thus the weakness of bond prices, has been a jump in inflation expectations. A market-based measure, looking at the relationship between inflation-protected Treasury bonds vs. the regular variety, has increased to levels not seen since the summer of 2015.

The short version of it all is that Trump’s fiscal stimulus plans -- coming so late in the business cycle with the unemployment rate already below 5 percent -- are likely to be highly inflationary, according to Capital Economics because inflation and wage growth “are already showing signs of accelerating.”

The firm estimates his proposed tax cuts would be worth up to $5 trillion over the next decade, while his infrastructure spending plans could come in around $1 trillion over five years. Add in a pledge to increase military spending, build the southern border wall and other proposals, and the economy is set to get a big push at a time when the labor market is near full capacity.

The result could be a more aggressive path of rate hikes by the Federal Reserve, further bond losses and higher borrowing costs for consumers.

Trump could blow up the national debt

As structured now, Trump’s plans are set to double the national debt, per the Committee for a Responsible Federal Budget, at a cost of nearly $12 trillion over the next 10 years. To stabilize the debt, according to the committee’s estimates, U.S. economic growth would need to clock in at 5.4 percent vs. the 2.1 percent growth projected. And to balance the budget under Trump, growth would need to come in at a whopping 10.3 percent.

Another option would be spending cuts, with a 27 percent drop in spending needed to stabilize the debt. Or some combination of higher growth and spending cuts. The trouble with this, however, is that if we only look at nonentitlement outlays beyond areas including Social Security and Medicare, federal spending would need to drop by half to merely stabilize the debt.

Add it all together, and unless growth more than doubles and nonentitlement spending drops by about a quarter, the national debt will continue to grow. With the debt ceiling needing to be raised by March, bond prices are weakening as traders realize the flood of borrowing will continue.

China and other nations are getting nervous

Another tenet of Trump’s economic plans is his call to renegotiate trade deals, label China a currency manipulator and potentially buy back or otherwise restructure the national debt at a discount. This has resulted in selling pressure in emerging market currencies and equities as investors worry about the economic impact to export-oriented nations.

Many of these nations have been aggressively selling their Treasury bond reserves, contributing to the falling prices and rising yields. Part of their motivation is a need to raise cash to defend their currencies in the open market. And part is the fear of sustaining losses from a Trump debt restructuring and/or higher inflation.

To be fair, the selling dynamic was in high gear before Trump won: Foreign central banks sold a record $346 billion worth of U.S. Treasury bonds in the 12 months through August. But the turnover in Washington will now only accelerate the trend.