Research reputations can be misleading

(MoneyWatch) The quest to find the best money managers leads many investors to look for those with the best research staffs. Two such companies that investors turn to are SEI and Russell. Have investors been well rewarded for trusting the research? Not according to the data.

Russell's Web site states: "When you work with Russell, you'll be collaborating with a global leader in money manager research. Our process uses quantitative and qualitative methods to choose the managers we think are the best worldwide. Of the 6,197 manager products continually monitored and researched, only 376 are assigned a role in a Russell product. We believe our extra depth of research and monitoring offers you a competitive edge."

- Should you be active in emerging markets?

- Are we clinging to failed strategies?

- Avoid the black hole of investing

SEI's Web site states that they provide "access to sophisticated investment strategies and top-tier money managers typically out of reach for individual investors." They add: "Using a robust process we call 'managing the managers,' we identify and hire specialist managers who have honed their investment styles and approaches."

Collectively, the assets under advisement or management are well into 10 figures. Obviously, people believe that Russell and SEI must be able to identify the future. However, their trust seems to be misplaced. For several years now I have been reporting on the results of their efforts. The last time I blogged on their performance was in February 2011, showing the results for SEI and for Russell over the period 2000-2010.

With two more years of data, it's time for an update. We'll compare the results of their funds to the passively managed funds of Dimensional Fund Advisors. (Disclosure: My firm, Buckingham Asset Management, primarily uses DFA funds in constructing client portfolios.) The results continue to be both amazing and consistent. Each time I have run the data, the results have been the same. Losing each time, and in every single asset class, is pretty hard to do, even if you set out to do it. Yet, SEI and Russell have managed this feat.

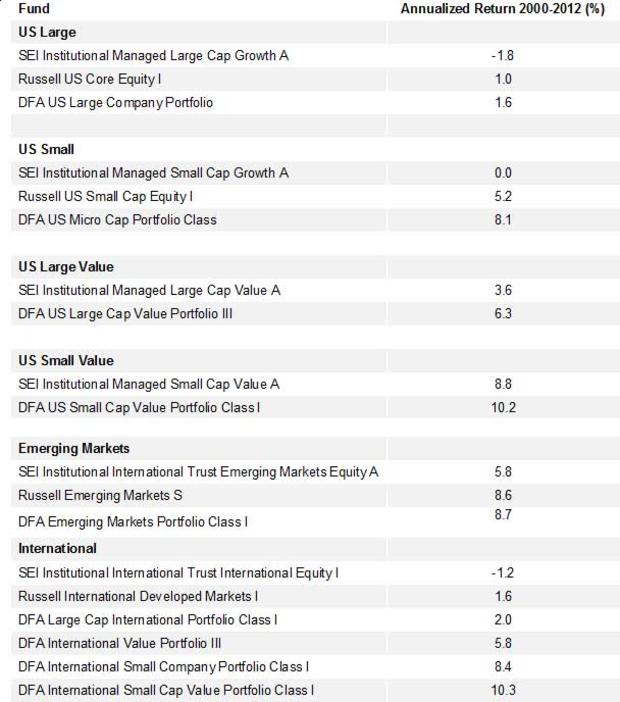

The following table presents the results over the period for which we have data for all of the funds, the last 13 years (2000-2012). Where more than one version of a fund is available, the lowest cost version is used. As you can see, the actively managed funds of SEI and Russell underperformed the passively managed funds of DFA in every single case. It didn't matter whether the asset class was large caps or the supposedly inefficient classes of small caps and emerging markets.

Using the DFA Large Cap International fund for that asset class (the DFA fund with the lowest return for the period), an equal-weighted portfolio of six DFA funds would have returned 6.2 percent. A similar SEI portfolio would have returned just 2.5 percent. That's an underperformance of 3.7 percent a year. (Disclosures: The returns of these portfolios don't include trading costs and advisor fees. My firm recommends each of the DFA funds used in these sample portfolios and doesn't build portfolios in the manners described in these sections.)

Russell vs. DFARussell only has funds in four of the asset classes. An equal-weighted portfolio of their funds would have returned 4.1 percent, underperforming by 1 percent a year an equal weighted portfolio of DFA funds (again, using only the DFA Large Cap International fund to represent that asset class) that would have returned 5.1 percent.

It is important to note that the underperformance of both fund families is well beyond the difference in their expense ratios, demonstrating that the cost of active management goes well beyond just the visible expense ratios of the funds.

Given the considerable resources that these fund families have at their disposal, the evidence demonstrates just how difficult it is for active managers to outperform the market. If these firms can't do it, what are the odds that you or your advisor can? This type evidence is why active management is called the loser's game. It's not that you can't win. It's that the odds of winning are so low that it isn't prudent to try.

Image courtesy of Flickr user 401(K) 2013.