How not to pay your bills

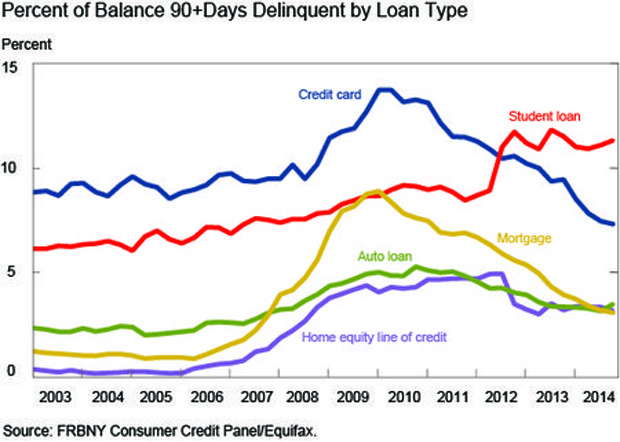

Americans increasingly are falling behind on their auto and student loans, new figures from the Federal Reserve Bank of New York show (see chart at bottom). If you're struggling to pay your bills, here's how you can contain the potential damage to your finances.

Contact your lenders. You may qualify for a loan modification or a temporary reduction in your payments. Federal student loan debt is particularly flexible, offering a number of repayment options. Those include a "Pay as You Earn" plan that can reduce your required payment to zero if your income is low. Auto lenders may let you skip a payment or even refinance your debt, depending on your credit scores and the lenders' policies. People resist calling their lenders, "but that's the wrong response," said Phil Reed, senior consumer advice editor for car site Edmunds.com. "They really don't want you to default... they really are trying to keep you in the game."

Understand the consequences. Even one skipped loan or credit card payment can devastate your credit scores, but how lenders report and react to delinquencies varies considerably. With an auto loan, for example, the lender can repossess your car if you're a single day late with a payment, although most wait until you're 30 days or more to start the collections process. Delinquencies on federal student loans, by contrast, typically aren't reported to the credit bureaus until you're 90 days overdue, and you're not considered in default until you're 270 days late. Even then, you have options to "rehabilitate" your loans and erase some of the credit history damage. Private student lenders aren't as forgiving -- many report delinquencies after 30 days and start collections soon after. Credit card issuers differ in how they react to delinquent debt, but after six months most send the debt to collectors.

Know what's at stake. Collectors going after defaulted federal student loans have extraordinary power to collect what you owe -- they can withhold your tax refund or take a chunk of your wages or Social Security payments, all without going to court. Collectors of private debt have to get a judge's permission for a wage garnishment and can't go after refunds or government benefits. Auto lenders can repossess your car and then sue you for any difference between what the vehicle is worth and what you still owe. If a repossession is in your future, turning the keys in voluntarily may not help your credit, but it can reduce the late fees, penalties and collection costs you otherwise would have to pay, Reed said.

Consider your next steps carefully. You may be tempted to let your student loans go unpaid while you try to keep up with your credit card payments. The problem with that approach is that credit card debt typically can be erased in bankruptcy, while student loans -- even from private lenders -- typically can't. If your credit card debt totals half or more of your current income, or you're struggling just to make minimum payments, you should talk to a bankruptcy attorney about your options. Likewise, if you really can't afford your car and can't sell it because you owe more than it's worth, a bankruptcy filing could erase what you owe your lender after repossession. This isn't a step to be taken lightly, of course, since bankruptcy can affect your credit scores for up to 10 years.

Set your priorities. In a financial crisis, you have to first make sure the essentials are covered, said consumer advocate Gerri Detweiler, Credit.com's director of consumer education. Groceries, utilities and keeping a roof over your head are most important. If you need your car to get to work, staying up on those payments is a necessity as well. Don't let lenders or collectors talk you into a payment plan that jeopardizes what you need to live.