3 ways to cut your investment tax bill

Are you paying a lot of taxes on your investments? Although it's too late to change your 2013 taxes, you can do a few things for 2014 and beyond.

First, buy tax-efficient investments. Mutual funds that turn over their portfolio pass through the taxable gains to their holders. Many active funds buy and sell stocks so frequently that their average holding period is less than a year. Investors get a 1099 from the mutual fund family showing they must recognize short-term and long-term capital gains.

Believe it or not, that can even happen in years when the fund value declined. A low-cost index fund such as the Vanguard Total Stock ETF (VTI) has very little turnover and allows the investor to control when and if she recognizes the gain.

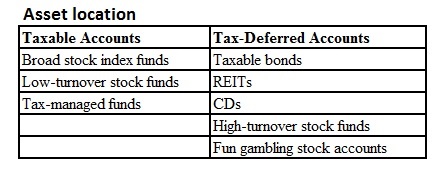

Second, locate your assets in a tax-efficient manner. Once you select an asset allocation, locate the assets so that you pay less in taxes. Tax-efficient vehicles, such as the index fund mentioned above, belong in your taxable accounts. Anything taxed as ordinary income -- such as bonds, CDs and REITs -- generally belongs in your tax-deferred accounts. The Roth tax-free wrapper is much more dependent on each investor's situation, but often a REIT works here since distributions are taxed as ordinary income and have more opportunity to grow than bonds.

I've always said investing is simple, but I've never said taxes are. There are a multitude of exceptions to the guidelines above in individual situations depending on variables such as current and future income, tax-loss carryforwards and the like.

Taxes are costs, too, and tax-efficient investing is critical to building a nest egg. We all like to pay less in taxes, but never forget that the much better goal is to make more money after taxes.