More U.S. students borrowing for college

(MoneyWatch) The number of U.S. students who borrow money for college continues to climb, while the number of graduates who are paying off these loans is slipping.

A new report by the Department of Education found that 64 percent of grads from the class of 2008 borrowed for college, compared with 64 percent for the class of 2000 and 49 percent for those graduating in 1993. The average amount that the students borrowed has continued to spiral up, rising from $14,000 in 1993 to $24,700 in 2008.

While the debt load was larger for the later graduates, they were less likely to have begun repaying their college loans a year after graduation. Sixty percent of 2008 grads were repaying their loans a year after receiving their degrees compared to 65 percent for the 2000 grads and 66 percent for the earliest grads in the study.

A larger number of the most recent graduates, at 31 percent, faced high monthly loan payments -- defined as amounts that were greater than 12 percent of their income -- than their counterparts who graduated in 1993 and 2000 (22 percent and 18 percent, respectively.)

Whether students borrowed for college was partially dependent on what type of institutions they attended. For the most recent graduating class that the report covered, 90 percent of students attending for-profit schools took out a loan, compared with 62 percent who graduated from public universities and 70 percent who attended private, nonprofit schools.

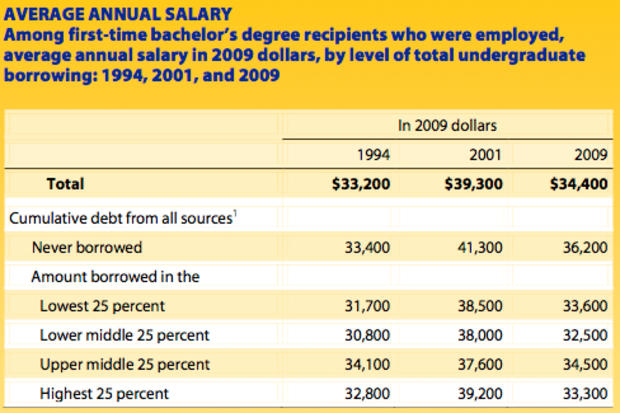

Eroding Salaries for New College Grads

While not a focus of the study, the government figures also illustrate how beginning salaries of new college grads have been eroding, which only makes the debt burden more onerous.

The average beginning salary of new college grads in 1994 was $33,200 (in 2009 dollars), and 15 years later the beginning average salary had only inched up by $1,200. And the new grads have actually lost ground since 2001, when the typical salary was $39,300. Students who never borrowed for college, presumably many from more affluent families, were earning the highest salaries in two out of the three time periods.

The researchers noted that high student loan debt, even for those who are able to pay off their loans, could hinder their ability to obtain a graduate degree, achieve financial independence from their parents and start their own families.

A safety net for college borrowers

While student debt can be scary, graduates who stick with federal college loans, which are the most popular type, have access to an often overlooked safety net.

Overwhelmed borrowers can qualify for a federal repayment plan that essentially allows them to pay based on what they are earning rather than on what they owe. The latest repayment program is called the Pay as You Earn Repayment Plan.