How life insurers can sell you a policy without a doctor's visit

We've all seen the advertisements for life insurance policies with "no medical exam necessary" on TV and the internet. Just answer a few basic questions online, provide access to your credit report and other personal information, and – bingo – you've bought yourself a $500,000 life insurance policy.

Such "no muss, no fuss" transactions are today a staple of the insurance industry. "This is the one thing that every life insurer sees as a major priority," said CEO Bob Kerzner of LIMRA, a research and development organization for the insurance industry.

But New York Gov. Andrew Cuomo and his Department of Financial Services (NYDFS) have a different priority. In a June letter to all insurers in the state, NYDFS said it wanted to know more about how life insurers are able to cover people without doing even a basic health check.

The answer may be that life insurers can infer a lot about how healthy you are by using so-called big data techniques that scoops a range of information. According to the NYDFS, that includes credit reports, purchasing habits at both stores and online, affiliations with churches or other groups, homeownership status and education.

Insurers then plus this data into an algorithm that spits out a yes/no or "charge more" answer when it comes to granting the policy.

Consumer advocates like Robert Hunter say this practice dangerous because it allows insurers to discriminate based on where a person lives, education attained, probable earnings, and even race or ethnicity. Hunter has been fighting against insurers that use the same kind of big data techniques in writing car policies instead of looking at driving records.

Many states have outlawed a formerly common practice in auto insurance known as "price optimization," in which car insurers search their databases for policyholders unlikely to switch carriers and then charge them more for each new policy.

"Much more needs to be done," said Hunter, head of the insurance department at the Consumer Federation of America in Washington, D.C. "State and federal regulators need to get on top of this."

The National Association of Insurance Commissioners (NAIC) is also investigating how insurers use consumer data, algorithms and "predictive analysis" for underwriting. And just this week, Minnesota forced Farmers Insurance to give back $315,000 to 1,600 auto insurance customers. The insurer charged them higher rates because they were renters rather than homeowners, an illegal practice in the state, according to state officials.

New York state's action is significant for two reasons. "It is the first state insurance regulator to directly examine life insurers' use of algorithms," said attorneys Mary Jane Wilson-Bilik and Tony Ficarrotta in the legal database Lexology. And it is one of the country's biggest markets for life insurance. MetLife, the largest domestic life insurer, is based in New York City, for example.

Auto insurers make no secret about why they use information like credit reports to reject those they deem to be bad drivers. A low credit score could indicate careless behavior both with money and on the road, they contend. By contrast, group affiliations, like religious ones that ban alcohol, make it less likely that a motorist could end up a drunk-driving casualty. Each insurer using this data has its own specific "scoring" devices.

Unlike auto insurance, life insurance is not mandatory, but many of the same rules apply. So Gov. Cuomo and the NYDFS could argue that the same rules of non-discrimination should also apply. If so, they'll be going head to head with a growing and lucrative practice used by insurers.

The old and cumbersome way of buying life insurance is about as relevant today as a rotary-dial phone. Filling out forms about your health and, more important, waiting at home for a paramedic to draw blood and a urine sample are considered passé.

According to LIMRA, which is funded in part by the insurance industry, an estimated 50 million people in the U.S. want life insurance. But 19 million (see chart below) wind up being "stuck shoppers," meaning they start the process but never finish because it's too cumbersome.

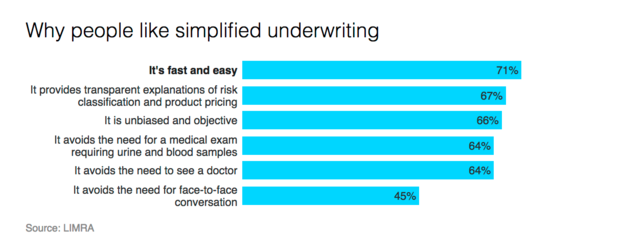

So would they do it without a medical exam? "Seven out of 10 said yes," according to Kerzner. In most instances, taking the physical is largely a waste of time because up to 95 percent of all candidates for a life insurance policy, either whole life or term, will qualify for at least a standard policy.

"As technology has evolved, companies are trying to find data sources and analyses that would reliably identify the bad risks," he said.

Kerzner also said that while regulators are concerned about privacy, most people just wanted to "streamline the underwriting process." The consumers LIMRA surveyed felt that this procedure was unbiased and not discriminatory, and liked the idea of a faster way to get life insurance, he said.

Still, regulators such as NYDFS have a lot of power, and insurers aren't going to openly challenge them. "The American Council of Life Insurers (ACLI) looks forward to providing assistance to the NYDFS on its information request," said the ACLI in a statement. "Our industry strongly supports consumer protections."

By providing information about internal documents, insurers are threading a very sharp needle. New York state is asking for proprietary company information about the kind of data the insurers gather; the names of vendors who provide it; a breakdown on how the information is used; if the client knows what's being done; their right to appeal; and whether the information is kept – or destroyed – once the policy is purchased. This would be valuable ammunition for industry competitors, as well as critics outside of it.

Meanwhile, Kerzner pointed out that big data is used everywhere. "This is a broader issue than just (insurance) underwriting," he said.