How to maximize your Social Security payouts

(MoneyWatch) One of the smartest things you can do to prepare for your retirement is to make your Social Security income as large as possible by delaying benefits for as long as you can (but no later than age 70). Seems simple, right? But according to the Social Security Administration, about half of all Americans start Social Security at age 62, the earliest possible age with the lowest income, and nearly three-quarters of Americans start before their full retirement age (FRA).

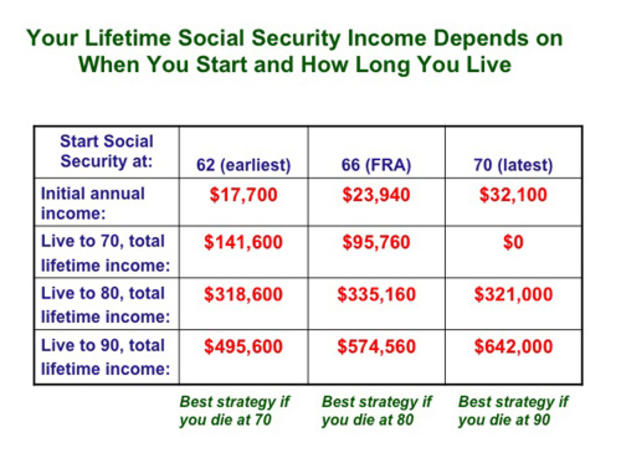

Let me show you why it makes sense to postpone starting your Social Security benefits. We'll take a look at people born in 1950 This year, those folks will turn 62 and become eligible for Social Security benefits. The following table shows estimates of the total lifetime Social Security income for a single person earning $75,000 per year in 2012 for three different starting ages: age 62, your full retirement age and age 70.

The first row shows projections of the initial annual Social Security income for the three different starting ages. I estimated these by using the Quick Calculator on the Social Security website. In this example, if you start Social Security benefits at age 62, your annual income would be $17,700. Your income increases to $23,940 if you wait until age 66, the FRA for people born in 1950. And if you wait until age 70, the oldest age at which you can start benefits, your annual income increases to $32,100.

The second row shows the total income you'd earn from Social Security over your lifetime if you live just to age 70 and then die. In this case, starting Social Security at age 62 is the best strategy, since the total lifetime income -- $141,600 -- is the highest. If you wait until age 70 to start Social Security income but then die at the same age -- well, that's a bad move, because then you get nothing.

The third row shows the total lifetime income if you live to age 80 and then die. In this case, starting Social Security at your FRA is the best strategy, because it provides the highest total lifetime income: $335,160.

The fourth row shows the total lifetime income if you live until age 90 and then die. In this case, starting Social Security at age 70 is the best strategy, since your lifetime income is highest at $642,000.

Note that these estimates are in current dollars -- the totals haven't been adjusted for the time value of money or to reflect future cost-of-living adjustments. Adding these refinements in the calculations only complicates matters but doesn't change the main conclusions.

The ideas in this post apply to single people; the considerations get more complicated for a married couple. However, it's usually the case that the best strategy is to have the highest wage earner -- often the husband -- delay taking Social Security benefits for as long as possible.

This table shows why it's good to have an estimate of your life expectancy. My earlier post, How long do you have to live, showed that the average age at death for Americans currently in their 50s and 60s is their mid-80s. This suggests that delaying Social Security benefits until FRA or beyond is the best strategy.

And keep in mind, these are just average life expectancies across the entire population. If you have above average education, above average income and you don't smoke, chances are good you'll live beyond the average life expectancy for the population at large. Your life expectancy also depends on your particular family history and the lifestyle choices you make. You can estimate your life expectancy taking these factors into account at the websites www.livingto100.com or www.bluezones.com.

Here are answers to a couple common questions -- and misconceptions -- about when to take your benefits:

Wait to take Social Security? No way! Take it as early as possible. After all, you never know when you'll die.

I can't tell you how many times I've heard that mistaken reaction to the ideas in this post. Yes, you don't know for sure when you'll die, but it's more likely you'll live close to your life expectancy or beyond, and the odds are pretty small that you'll die in the next few years.

I don't need the Social Security income, but I'll start it early anyway and invest the money.

Another bad idea for most people. To win this bet, you'll need to die early, or take a lot of risk in the stock market.

One of the best ways to determine when to start your Social Security benefits is with online software that analyzes the decisions that will give you the largest lifetime payout. Examples include www.socialsecuritytiming.com and www.socialsecuritysolutions.com.

Boost your Social Security payout by $100,000

Social Security strategies: How to get $90,000 more for your spouse

Start Social Security early and invest? Ask the actuary

It may take a few hours to analyze the information and determine the best age for you to start collecting Social Security, but it can increase your lifetime payout by thousands of dollars. In effect, you'll be paying yourself hundreds or thousands of dollars per hour for the time you spend doing your homework now. That's a pretty good return on your investment!

Image courtesy of iStockphoto contributor Kameon007.