Are U.S. stocks too expensive?

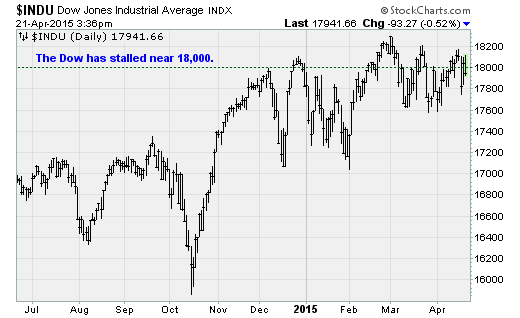

The Dow Jones industrial average continues to struggle near the psychologically important 18,000 level -- a hurdle first cleared back in December. For the last five months, equities have been spinning their wheels trying to find traction.

Foreign stocks, however, have been on a roll. The Shanghai Composite is up by nearly a third over the same period. Japan's Nikkei Average is up nearly 18 percent. Germany's DAX is up nearly 30 percent.

There are many reasons for the divergence in performance. In the U.S., the Federal Reserve is expected to raise interest rates later this year for the first time since 2006; by contrast, central banks overseas continue to unveil or hint at new stimulus measures. Currencies also have been a factor, as has a turn in the economic data, with the U.S. disappointing of late while Europe improves.

But growth in corporate earnings, and thus valuations, is likely the main dynamic. After enjoying a surge of profitability out of the recessionary low, corporations have had to contend with the drag of the stronger dollar (crimping foreign earnings), lower energy prices (slamming the top-line growth of oil and gas companies), and a tightening in the labor market (which is expected to result in wage cost pressure later this year).

Capital Economics notes that aggregate operating profit margins for companies in the S&P 500 fell from a record high of 10.1 percent in the third quarter of 2014 to 9 percent in the fourth quarter. A further slide is expected if the dollar remains strong and the U.S. job market keeps tightening. The latter, according to the research firm, will result "in a larger share of revenue finally flowing to workers at the expense of the owners of capital."

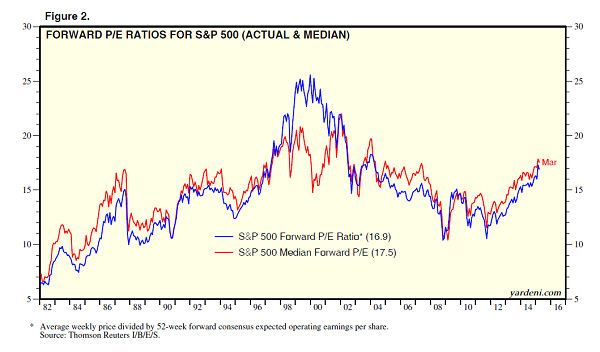

The fact that stocks have remained aloft despite the earnings slowdown has pushed up valuation metrics. Ed Yardeni of institutional advisory firm Yardeni Research worries that they've entered "the outer limits of rational exuberance and [are] bordering on irrational exuberance."

Stock market valuations have floated up to the highest levels since the start of the current bull market. As the chart above shows, the S&P 500's forward price-to-earnings ratio has returned to levels not seen since 2004.

In interviews with institutional clients, Yardeni finds that most seemed to agree that stocks are "frightfully overvalued, if not frighteningly so." Moreover, almost none of them are trying to justify these valuations with structural factors like below-target inflation and ultra-low interest rates, factors that have historically made stocks more attractive and thus more expensive. Skepticism reigns.

Instead, they're saying that if stock prices move higher from here, it would be because of a melt-up stock bubble driven, in Yardeni's reasoning, by corporate share buybacks. Companies repurchased more than $2 trillion worth of stock between 2009 and 2014. By comparison, this year alone companies are on track for $1 trillion in buybacks, versus $553 billion last year.

Whether these price-insensitive corporate buyers this will be enough to overcome the drag from lower earnings and the threat of higher interest rates remains an open question. For now, the battle will likely continue near Dow 18,000 until the Fed pushes back the timing to hike rates.