Why not just buy stock in Berkshire Hathaway?

(MoneyWatch) Recently, after giving a speech based on my latest book, Think, Act, and Invest Like Warren Buffett, I was asked a question that I've often received over the years: Instead of building your own globally diversified portfolio, why not just buy the stock of Buffett's company, Berkshire Hathaway (BRK.A)? The question reminded me of a bit of research I did when asked the same question about seven years ago.

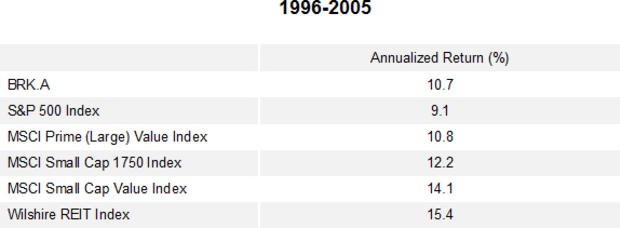

Back then, I suggested the following to the person who asked the question first. Let's take a time machine back to January 1, 1996 (remember, this was back in early in 2006): You inherited a large sum of money and decide that based on Buffett's spectacular track record you will invest it all in BRK.A. Over the next 10 years (1996-2005), BRK.A returns a healthy 10.7 percent. The table below shows the returns for the five major U.S. equity asset classes over that same period.

You'll note that the BRK.A outperformed only one of the five major U.S. equity asset classes. In addition, an equally-weighted (20 percent each) portfolio of the five asset classes, rebalanced annually, would have returned 12.7 percent, outperforming BRK.A by 2 percent a year. Ten years of underperformance would test even the most disciplined, patient investors. The typical institutional investor reviews performance on a three-year cycle. Thus, even if Buffett went on to outperform in the future, it's likely that most investors wouldn't have been around to benefit.

To bring us up to the present, the table below updates the data to cover the period January 1996 through September 2013.

Over this 17 3/4-year period, BRK.A underperformed three of the five major U.S. asset classes -- although it did outperform the equally-weighted, annually rebalanced portfolio by 0.2 percent. That's not much of a difference, and it certainly wouldn't earn someone the title of "Oracle of Omaha."

Back in early 2006, I explained to that first questioner that, while Buffett probably had the greatest track record of any investor, we only know about his great performance in hindsight. Forty years earlier, there was no way to know that he would turn out to be the greatest investor of his generation. And, while there have been many investment managers who have tried to mimic Buffett's results, few have come close to replicating them.

That raises the question: How long does one wait until you're sure that an investment manager's track record is based on skill, not luck? A related problem is that by the time you can be confident that the manager's results are skill-based, not just the result of a lucky outcome, he's probably managing a much larger amount of assets, which makes it harder to outperform. A third problem can arise if a manager goes through a period of poor performance. Exactly how long do you hang in there before deciding that either he has lost his touch or that increased assets under management have become too great a burden?

Tomorrow will take a look at some important issues you should consider before deciding to invest in BRK.A.

Image courtesy of Flickr user Tax Credits