How did these "sure things" fare in 2013?

This is our final review of 2013’s “sure thing” predictions. Keep in mind that if they were sure things, they should all (or at least most of them) have come true. As is our practice, we give a score of +1 for a forecast that can true, a –1 for one that was wrong and a zero for one that was basically a tie.

The golden age of stock investing is over.

Reasons that stocks wouldn’t do as well in the future included:

- Demographics (shifting from stocks to bonds as we get older and more conservative)

- America's fiscal problems

- Currently high valuations (the Shiller CAPE 10 was almost 23 at the start of the year)

It would be hard to have gotten this one more wrong, with the S&P 500 returning 32.4 percent. Score: -1

Fast growing economies will provide the best results.

Another sure thing was that Europe's recession and the slow growth in the U.S. would mean that the highest returns would come from the fastest-growing economies, specifically China. European stocks should be avoided.

While China’s economic growth has slowed from double digits, it still grew at about 7.6 percent in 2013. That’s more than four times as fast as the estimated 1.7 percent rate for the U.S. economy. Despite the differences in growth rates Vanguard’s 500 Index Fund (VFINX) gained 32.2 percent while the China ETF FXI lost 2.2 percent, an underperformance of 34.4 percent. As to Europe, Vanguard’s European Index Fund (VEURX) returned 24.7 percent, or more than twice the long-term compound return on stocks. Score: -1

Inflation will rise.

The third sure thing was the inevitable rise in inflation due to the fiscal and monetary stimulus that continues to be injected into the economy.

The current full year forecast for the CPI in 2013 is just 1.4 percent, actually down from 2012’s low rate of 1.7 percent, which was lower than 2011’s rate of 3.0. Score: -1Investors should keep bonds short-term.

Another certainty was that investors should limit the maturity of their bond holdings to the very short term. This was a good call. Vanguard’s Short-Term Bond Index Fund (VBISX) only returned 0.1 percent, but that was better than the losses experienced by its Intermediate-term Bond Index Fund (VBIIX, -3.5 percent) and its Long-term Bond Index Fund (VBLTX, -9.1 percent). Score: +1

The price of gold will soar.

The fifth sure thing was that the Federal Reserve's easy monetary policy and rising inflation would send the price of gold soaring.

We have another loser here as gold plunged from $1,658 an ounce to $1,205 an ounce. Score: -1

In the U.S., the best returns are from equity investments with higher yields.

The sixth sure thing was that you should seek the "safety" of investments with higher yields -- such as high-dividend stocks, master limited partnerships and real estate -- for domestic stocks.The Vanguard 500 Index Fund (VFINX) returned 32.2 percent.

In doing so it outperformed Vanguard’s SPDR S&P Dividend ETF (SDY), which returned 30.1

percent; the ALPS Alerian MLP ETF (AMLP) which returned 18.6

percent; and Vanguard’s REIT Index Fund (VGSIX) which returned 2.3

percent. The average of the three “alternatives” was a return of 17 percent, or

15.2 percent below that VFINX’s return. Score: -1

Investors should own Apple stock.

The road to riches this year was supposed to be through owning Apple (AAPL) shares.

The stock began the year with a P/Eof just 11.4, compared to about 15 for the overall market. While the S&P soared 32.4 percent, Apple returned just 7.6 percent, an underperformance of 24.8 percent. Score: -1

It’s a stock-picker’s year.

Our eighth sure thing was that it will be a year when active fund managers outperform their benchmarks.

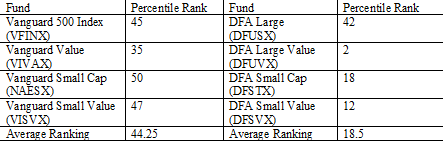

Correlations did fall. However, that didn’t help active managers, who must now go looking for another excuse. The following table shows the Morningstar percentile rankings for Vanguard’s index funds and Dimensional Fund Advisors passively managed asset class funds in the four major domestic asset classes. You’ll note that not in a single case did the majority of active funds outperform any of the Vanguard or DFA funds. Score: –1

Total Score: –7/+1

Of eight predictions, only one

turned out to be correct. Soothsayers and palm

readers likely would have done better. Unfortunately, this type score isn’t unusual.

This was the fourth year we’ve tracked a range of sure things, and not once have even a

majority proven to be accurate forecasts.

The

historical evidence demonstrates that there really are no good market

forecasts. Yet millions of investors will be basing their

investment decisions on the prognostications of so-called gurus. And you can be

sure that the well-known confirmation bias will be at work — investors are more

likely to believe and act on a forecast that agrees with their own beliefs.

You don’t have to make that mistake. The strategy most likely to allow you to achieve your goals is to have a well-developed and written investment policy statement, including an asset allocation and rebalancing table, and adhere to it — ignoring not only all forecasts, but the “noise” of the market as well.

Before closing we need to review my own two forecasts, which were that actively managed funds will lose market share to index funds and exchange-traded funds and that broker-dealers will lose market share to registered investment advisors. Both of those came true, but I won’t take any credit for getting them correct because they were as sure as the sun rising in the east.