Could the Fed's next move be ... negative rates?

In a massively hyped Federal Reserve policy announcement Thursday, one that threatened to end the almost seven-year experiment with near-zero percent interest rates with the first rate hike since 2006, Janet Yellen and her cohorts delivered a dovish result: A no hike decision, in line with futures market odds.

Yet, stocks surprisingly drifted lower. The nagging fear is that maybe the ultra-easy monetary policy the Fed has had in place since 2008 isn't enough.

If so, investors will need to change their focus.

The Fed's Summary of Economic Projections, or "dot plot," revealed that at the median Fed officials now expect only a single rate hike by the end of 2015. The futures market is now pricing in a 49 percent chance of a hike at the December meeting.

The kicker -- the one that apparently pushed large-cap stocks lower into the closing bell -- was the appearance of a negative interest rate projection on the dot plot.

Some Fed policymaker (dot plot estimates are anonymous) now expects the federal funds policy rate to fall into negative territory by the end of this year and remain so through the end of 2016. Moreover, four officials don't expect any hikes this year at all. In her post-announcement press conference, Yellen admitted that the Fed was "way below" its inflation target.

RBS' Alberto Gallo railed in a note to clients that he was "Fed up with the Fed" and admitted he didn't think keeping rates low would spur inflation and allow Yellen to hit her target.

He explained: "It has not worked so far, indicating low inflation could be structural, owing to sectoral labor market slack, stagnant wages, technological advancement and unfavorable demographics on top of external pressure from commodities."

With corporate profits rolling over and global growth stagnating, people are wondering: Is this all the Fed and its cohorts can do? Fresh threats, such as another debt ceiling showdown in Washington this autumn and an election in Greece, are approaching.

All of which raise the odds that we could, in fact, see short-term interest rates in the U.S. move below the zero bound and into negative territory -- something that has already happened in Europe.

For stocks, it will be critical for the bulls to recover from Thursday's intra-day sell-off. The day's action resulted in a very negative "shooting star" technical pattern -- indicating that higher prices brought out the sellers instead of encouraging new buyers. That signals speculative exhaustion and often precedes pullbacks.

Until fundamentals like retail sales and earnings turn higher again, restoring confidence in the Fed's ability to respond to economic turbulence from China and elsewhere, it will likely be difficult for equities to mount a sustained uptrend.

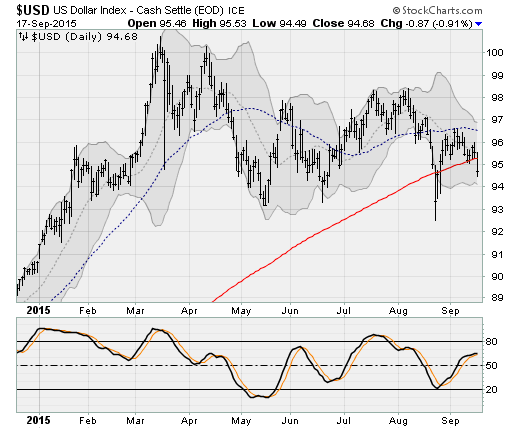

Better opportunities will likely be found in areas more directly affected by the specter of a more dovish Fed. This includes anything sensitive to the valuation of the U.S. dollar, which dropped 0.9 percent on Thursday back below its 200-day moving average -- a measure of medium-term trend. That level was last crossed during the "Black Monday" sell-off of August 24.

The prime candidates are commodities like precious metals and crude oil. Equity-only investors should consider beaten-down gold mining stocks and energy companies. The Market Vectors Gold Miners (GDX) gained 2.7 percent on Thursday to challenge its 50-day moving average for only the second time since May. The Energy Sector Select SPDR (XLE) looks ready to break out of a downtrend that started in early May, which took the fund down nearly 30 percent into its late August low.

The outlook for bonds is more difficult. Near-term bonds rallied hard as the threat of an imminent rate hike faded. Two-year Treasury yields collapsed the most since 2009. But long-term bonds have been under pressure in recent weeks as a more dovish Fed bolsters market-derived inflation expectations.

If you're a consumer looking at getting a loan, now is likely the time to lock in rate because any experiment with pushing short-term rates into negative territory would push long-term rates higher on the expectation of labor market overheating and rising inflationary pressure.

Indeed, Paul Ashworth at Capital Economics warned that "rising wage and price inflation next year will eventually force the Fed to tighten policy much more aggressively" given the labor market is close to full employment.

In his words: "The longer the Fed delays now, the higher interest rates will eventually have to go."