What's Your Tax Bracket?

This story was updated on March 1, 2011.

Pop quiz: What's your tax bracket?

If you don't know which of the six brackets you're in, you're in good company. But you could be making some money goofs or paying too much in taxes as a result. "Figuring out your tax bracket is very simple," says Gil Charney, tax analyst at The Tax Institute at H&R Block. "And that number is key to every tax-related decision you make."

- The $400 ($800 if married filing jointly) Making Work Pay Credit will expire.

- The Social Security payroll tax rate will decrease by 2 percent, to 4.2 percent from 6.2 percent, for wages up to $106,800.

- The self-employment tax will decrease by 2 percent, to 10.4 percent from 12.4 percent, on self-employment income up to $106,800.

- The estate tax will return with a rate of 35% and a lifetime exclusion of $5 million for 2011 and 2012.

- The personal exemption amount will increase to $3,700 (from $3,650 in 2010).

- The 2011 standard deduction will be:

--$5,800 for unmarried taxpayers or married taxpayers filing separately

--$11,600 for married taxpayers filing jointly

--$8,500 for taxpayers filing as head of household.

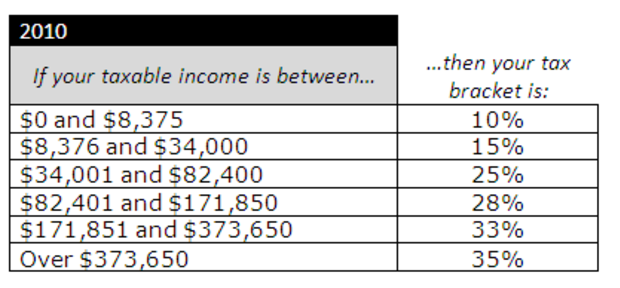

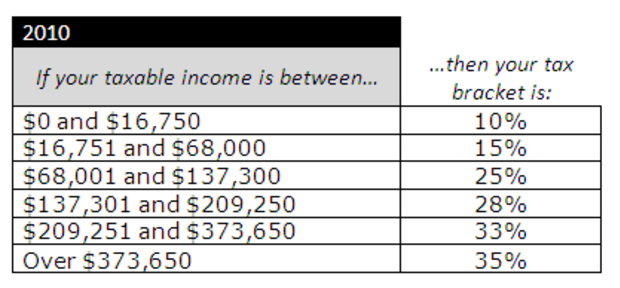

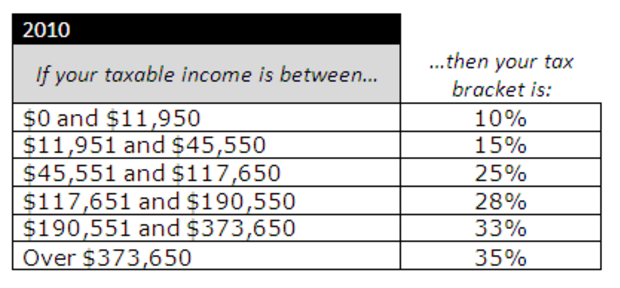

A quick tutorial: The U.S. tax system has graduated rates, which means you pay low tax rates on the first dollars you earn and progressively higher rates as your income goes up. If you file taxes jointly with your spouse, the first $16,750 you earn in 2010 is taxed at 10 percent; the next $51,250 is taxed at 15 percent; the next $69,300 at 25 percent and so on. The highest rate you pay is your marginal tax rate, often called your tax bracket.

Below, we’ve produced a full list of 2010 tax brackets for single people, married filing jointly and head of household. (Head of household status means you were unmarried on December 31, paid more than half the cost of keeping up your home, and a “qualifying person,” such as a child, lived in your home more than half the year.)

On December 17, 2010, the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 was signed into law. The law basically extended everything that was in place for another year.

Here are some of the differences for tax year 2011:

Once you’ve figured out your bracket from these tables, you can better tackle the financial questions that follow.

Filing Status: Single

Filing Status: Married filing jointly

Filing Status: Head of household

1. Should you buy a municipal bond fund or a taxable bond fund?

There has been quite an uproar recently in the municipal bond market. It started when experts and analysts questioned the ability of fiscally depleted states and municipalities to repay their bond obligations in the aftermath of the Great Recession. The anxiety of bond-holders skyrocketed after analyst Meredith Whitney went on 60 Minutes and predicted widespread defaults in the municipal bond market. (Here is a great primer on munis; here is how a municipal default would work and here is a rebuttal to Whitney’s central thesis.)

Since that time, municipal bond prices have dropped, causing individual investors to question whether these assets deserve a place in their portfolios. Here’s a reminder of why municipal bonds might be worth considering.

Municipal bond interest is exempt from federal income taxes (and in some cases state taxes), but it generally make sense to buy a muni bond fund only if you’re in a high bracket. Otherwise, you might earn more, on an after-tax basis, with a taxable corporate or government bond fund.

Say you have $10,000 to invest and you’re choosing between a muni fund yielding 3 percent and a taxable corporate bond fund yielding 4.5 percent. The muni fund will produce $300 in tax-free income. If you’re in the 25 percent bracket, you’d earn more with that taxable fund: $338 after taxes. But if you’re in the 35 percent bracket, a muni fund would be a better bet because its $300 tax-free payout beats the $293 you’d earn after taxes with the taxable fund.

If you live in a high-tax state such as New York or California, buying a single-state muni fund can be even more beneficial since you don’t pay state or federal income taxes on the income.

To compare yields on taxable versus tax-exempt funds, calculate the muni fund’s taxable-equivalent yield — that’s the yield a taxable fund would have to pay to produce the same after-tax income. The formula is the muni yield divided by (1 minus your tax bracket)/100. You can use online calculators such as Vanguard’s to do this math.

2. Should you pay off your mortgage?

As a rule, the higher your tax bracket, the less money you’ll save by prepaying your mortgage. Reason: The higher your bracket, the more your mortgage interest deduction is worth to you. Say you have a $300,000, 30-year, 5 percent fixed-rate mortgage and are consider sending the bank an extra $100 a month from day one. You’d save $39,938 in interest over 30 years. Subtract the value of your mortgage interest deduction, however, and you’d wind up saving $29,954 over 30 years if you’re in the 25 percent bracket but only $25,960 if you’re in the 35 percent bracket. Rather than using after-tax money to pay down their mortgage, high earners are better off boosting their pre-tax 401(k) contributions, where the money will grow tax deferred.

MoneyWatch editor-at-large Jill Schlesinger contributed to this article.

More on MoneyWatch: