What's a fair tax rate? It depends

How progressive should the U.S. tax system be? Answering this question requires an assumption about what's fair in terms of tax burdens across income groups. But people differ widely on what they consider fair. Therefore, fairness isn't something economic theory can address. Instead, a principle of fairness must be assumed.

For example, the tax literature offers many ways to assess tax burden equity across income groups. Under the principle of "absolute equity," everyone pays exactly the same percentage of income, no matter what his or her total income is. In this case, taxes would be flat rather than progressive.

Under the "benefit principle," an individual's tax burden is equal to the value of the government-provided goods and services the individual consumes (which is very difficult to calculate). If the rich are willing to pay more for services than the poor, or if the rich use more services than the poor (e.g. airports, police protection of businesses and homes, museums, performing arts centers and so on) than progressive taxes are justified on this basis. But if the reverse is true, and the poor use more resources than the rich, then the benefit principle points to a regressive tax structure.

The most popular justification for progressive taxes relies on the "ability to pay" principle. Under this definition of equity, the "pain" that each person experiences when paying taxes is the same.

One variant is the "equal marginal sacrifice" principle. It implies that the pain of giving up the last dollar of taxes is equal across income groups. For example, when a poor person pays the last $100 in taxes, it might require giving up a necessity like a pair of shoes for a child. But a high-income person might have to give up only a luxury rather than something essential for well-being. So the burden would be unequal.

The implication is that taxes for the wealthy should be increased, and taxes for the poor should be reduced until both sacrifice equally when they pay the last dollar of taxes.

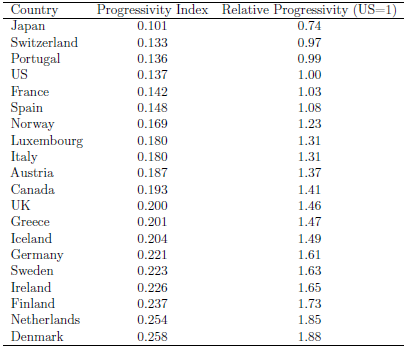

Recent research (nontechnical summary) examines the progressivity of income taxes on wages across 20 countries. This table summarizes the results:

The first column shows the degree of progressivity according to an index the authors, economists Hans Holter, Dirk Krueger and Serhiy Stepanchuk, developed. A larger number implies a more progressive tax system. The second column shows the degree of "relative progressivity," with the U.S. defined as 1.0 (that is, it's the ratio of a country's progressivity index to the index for the U.S.).

According to this analysis, taxes on wage income in the U.S. have a relatively low degree of progressivity. One rationale for this comes from supply-side economics, the idea that lower taxes on the wealthy will spur economic growth. However, little evidence supports the claim that growth rates in the U.S. have been higher as a result of "trickle down" tax cuts on the wealthy in the past. So, this economic argument doesn't hold up when compared to the evidence.

Is progressivity in the U.S. too low? The degree of progressivity in U.S. taxes -- the question of whether the current distribution of tax burdens is fair -- must be decided in the political arena. Economists can predict what might happen to GDP, prices, employment, etc. when taxes are changed, although as supply-side tax cuts show, those predictions are often unreliable.

But economists cannot say whether it's more or less fair to take a dollar from one person and give it to another (in effect what changing the degree of progressivity does). That's for all of us, through our political representatives, to decide.