The growing threat from falling business spending

The U.S. economy continues to underperform, demonstrating all the vitality and verve of a middle-aged couch potato.

On Friday, we learned that first-quarter GDP growth was upwardly revised to 0.8 percent, but that still missed expectations. The figure was dragged down, in large part, by a 6.2 percent drop in business fixed investment. Consumer spending growth, at 1.9 percent, wasn't enough to overcome this drag.

This isn't exactly surprising. Corporate earnings have been a disaster zone, hammered by weak commodity prices, the post-2014 energy decline and uneven retail results. The trouble is: If the slowdown in capital spending by businesses continues, it could result in a self-reinforcing downward spiral that puts the larger economy at risk.

With 98 percent of S&P 500 companies having reported by now, first-quarter earnings dropped 6.7 percent over last year, according to FactSet. This was the fourth consecutive quarter of falling profitability, something that hasn't happened since the recession ended. Overall S&P 500 revenues have declined 0.7 percent over the last 12 months -- only the second time this has happened in the last 12 years.

This weakness has, in turn, begat further weakness.

Peter Boockvar at Lindsey Group notes that nondefense capital goods orders, excluding aircraft, fell 0.8 percent in April over March -- well below the 0.3 percent growth that was expected. On year-over-year basis, core capital spending is down 6.7 percent and has fallen, on an absolute-dollar basis, back to levels not seen since 2011. And the rate of change had dropped to a pace not seen since 2006.

The worst-affected areas include machinery (mainly, mining and oil and gas industries), electrical equipment and primary metals -- the very building blocks of economic growth.

Currently, expectations are very high for a bounce-back in the second quarter. The Atlanta Fed's GDPNow real-time tracking estimate of second-quarter GDP growth stands at 2.9 percent, up from 2.5 percent on May 17, thanks to strong net exports and durable goods orders.

Still, in a recent note to clients, Goldman Sachs economist Jan Hatzius warned that the soft patch in capital spending has, like a metastasized cancer, spread to other areas of the economy. Spending in nonenergy equipment and intellectual property products (such as software, research and development, and entertainment-related items) fell between 4 and 5 percentage points over the last four quarters.

While a far cry from the 70 percent drop in spending on drilling-related structures since that category's peak, it's still worrisome.

And earnings, which are the raw fuel that powers capital investment and thus GDP growth, remain weak.

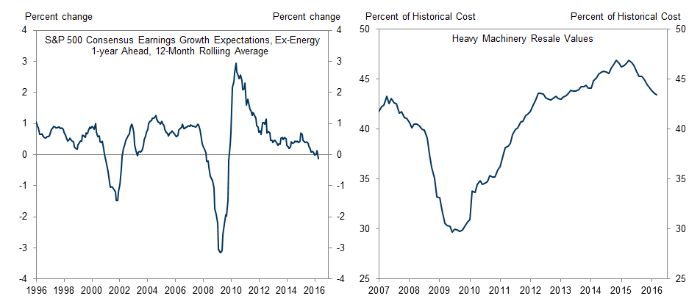

Consider this chart (above, left) of S&P 500 earnings expectations (minus energy), which have fallen into negative territory for the first time since the recession ended. Other factors, such as sliding values for used heavy machinery (above, right), also suggest overcapacity and declining machine utilization rates.

With less machinery and factory equipment being used, and prices falling, why order new? That'll drag on companies like Caterpillar (CAT) and could soon pull down GDP growth expectations, potentially rattling stock investors.