Declining profits could signal a market top

Last week, I discussed one of the primary drivers of the stock market rise over the last few years: Companies issuing low-interest debt and using it to buy their own stock. I think of it as a conveyor belt of capital from bonds into equities via corporate share buybacks. With credit so cheap, and corporate profitability at a record high, it's all been good.

Buybacks reduce the number of shares outstanding, boosting the all-important earnings per share calculation. And investors have rewarded companies for leveraging up their balance sheets like this. Capital Economics notes that the S&P 500 Buyback Index, which measures the performance of the 100 stocks in the index with the highest buyback ratios, has nearly doubled since the beginning of 2008 compared to a 30 percent gain for the overall S&P 500.

But now, the evidence is building that this dynamic -- arguably the "bubble" area of this bull market -- is beginning to end after corporate profits suffered their steepest fall in the first quarter since the financial crisis.

Investors are apparently beginning to sniff out trouble. So far this year, the Buyback Index is lagging the overall market.

It's becoming increasingly clear that record corporate profitability is unsustainably high and boosted by factors that cannot continue such as labor productivity, which has turned lower as the job market tightens. You can see this in the way that domestic non-financial corporate profits to gross value added has surged to the highest level in 63 years according to new data from the Bureau of Economic Analysis (BEA).

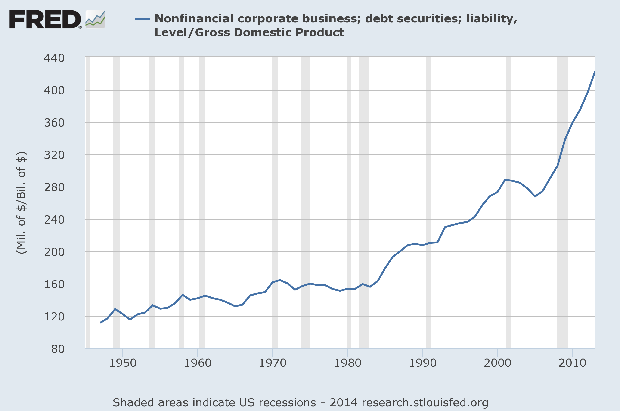

Corporate leverage is becoming a problem. Just look at the chart (above) of corporate non-finance debt as a share of the overall economy. Helped by the Federal Reserve's ultra-low interest rate policy -- and the fact that short-term interest rates have been near zero percent since 2008 -- CEOs have loaded up on debt.

So far, that hasn't mattered as healthy corporate profits have protected balance sheets and kept credit ratings high. Unfortunately, corporate profits are now faltering.

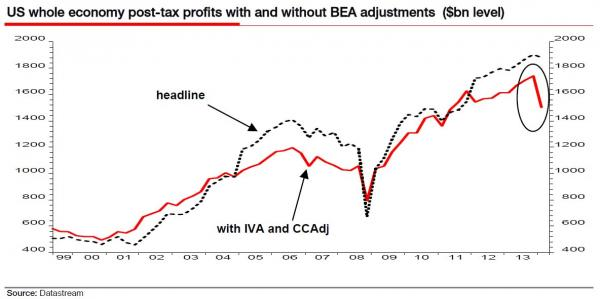

According to the BEA, whole economy profits dropped $213 billion in Q1 for a 10 percent annualized decline. Yet the overall market isn't really talking about this yet because of the adjustments government statisticians then make to the underlying data, removing profits from inventories and accounting for depreciation on an economic instead of a tax basis. As a result, as you can see in the chart above, the headline profits trend is a lot less scary.

Societe Generale analyst Albert Edwards notes that the large disconnect is being driven by the expiration of investment tax credits that allowed companies to lower their effective tax rates by accelerating the pace at which they could offset profits with deprecation expenses. As a result, less depreciation is being recognized and effective tax rates are rising, weighing on "real" profits and pinching corporate cash flow.

If this continues into the second quarter and beyond, it will make all that corporate leverage harder and harder to maintain. In turn, we should start seeing measures of balance sheet health like debt-to-equity start deteriorating. That will push up corporate borrowing costs. And that, in the end, will slam the door on the debt-to-equity conveyor belt that's been relentlessly pushing stocks higher.

The takeaway is to watch corporate profits carefully in the months to come. Like housing affordability and mortgage origination measures back during the housing bubble, a sustained turn lower in profitability could very well signal the top of this five-year-old bull market.