More people are delaying Social Security benefits

It looks like people are now paying attention to the plethora of advice retirement analysts and writers -- including me -- have been offering about delaying Social Security benefits as a means of improving retirement security. The Social Security Administration's Annual Statistical Supplement for 2013 provides evidence of a slow but steady increase since 2004-2005 in the age at which Americans start taking Social Security benefits, reversing a prior trend of claiming payments at earlier ages.

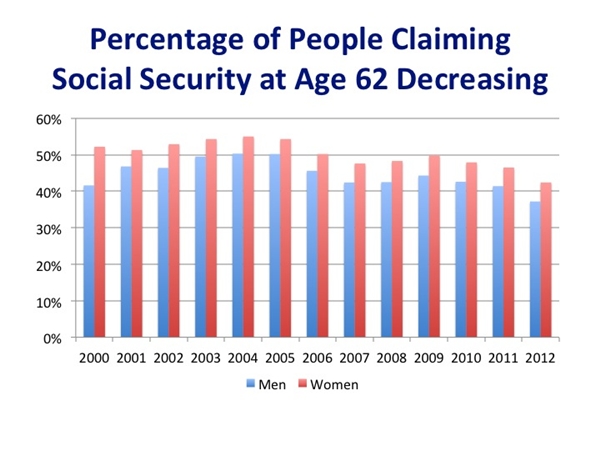

Age 62 is the earliest possible age to start collecting Social Security benefits, but it results in the lowest possible monthly income. The first chart below shows that in 2000, 41.6 percent of new Social Security awards for men were for 62-year-olds. This percentage climbed to 50.3 percent by 2004, but dropped to 37.2 percent by 2012.

Similarly, in 2000, 52.2 percent of new Social Security awards for women were for 62-year-olds. This percentage climbed to 55 percent by 2004, but dropped to 42.4 percent by 2012.

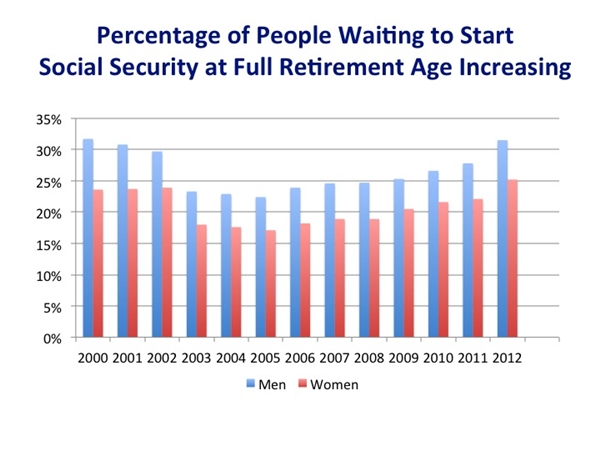

Your benefit is not reduced if you retire at your Full Retirement Age (FRA), which is 66 for people retiring today. The next chart shows that in 2000, 31.7 percent of new awards for men were for those who waited until their FRA to start benefits. This percentage dropped to 22.4 percent by 2005, but since has increased to 31.5 percent by 2012.

Similarly, in 2000, 23.6 percent of new awards for women were for those who had reached their FRA. This percentage dropped to 17.1 percent by 2005, but since has increased to 25.2 percent by 2012.

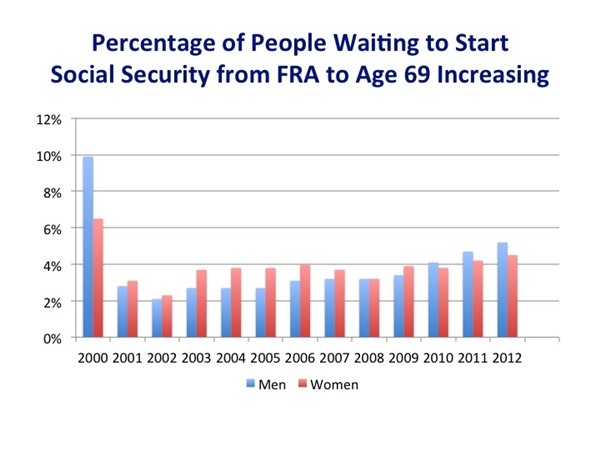

Your Social Security retirement income increases for every month you delay starting benefits after your FRA -- until you reach age 70, beyond which there are no further increases. The final chart shows that in 2000, 9.9 percent of new awards for men were for workers between their FRA and age 69. This percentage fell to 2.7 percent by 2005, but increased to 5.2 percent by 2012.

Similarly, in 2000, 6.5 percent of new awards for women were for workers between their FRA and age 69. This percentage fell to 2.7 percent by 2005, but increased to 5.2 percent by 2012.

The reasons for this slow but steady trend to delay Social Security benefits aren't clear. It could be that more people are hearing and heeding the messages about the advantages of doing so. It could also be that more workers are delaying retirement due to an improving economy -- the percentage of workers claiming Social Security early tends to rise when the economy is poor and fall when the economy improves.

Also, more people are reporting recently that they want to delay retirement, either due to the desire to continue working or because some people are making a realistic assessment that their retirement resources aren't adequate to support their lifestyle.

There are significant financial advantages to delaying the start of your Social Security benefits. This trend is encouraging to people like me who worry about Americans' retirement security. I hope it continues.