How to diversify your investments

(MoneyWatch) This post is based on chapter 6 of Larry Swedroe's new book Think, Act, and Invest Like Warren Buffett. The data for today's post and the associated text have been updated through the end of 2012.

Because most investors have not studied financial economics and don't read financial economic journals or books on modern portfolio theory, they don't have an understanding of how many stocks are needed to build a truly diversified portfolio. To effectively diversify the risks of just the asset class of U.S. large-cap stocks, you would have to hold a minimum of 50 stocks. For U.S. small-cap stocks, the figure is much higher. Once you expand your investment universe to include international stocks, it becomes obvious that the only way to effectively diversify a portfolio is through the use of mutual funds.

However, even when individuals invest in mutual funds, they typically don't diversify effectively because they make the mistake of thinking that diversification is about the number of funds you own. Instead, it's about how well your investments are spread across different asset classes. For example, an investor who owns 10 different actively managed U.S. large-cap funds may believe that he is effectively diversified. While it's true that each fund will likely have some differentiation in its holdings from the others, collectively, all the investor has done has been to create an expensive "closet" index fund. The reason is that it's likely that the return of his portfolio, before expenses, will approximate the return of an S&P 500 Index fund. After expenses, the odds are great it will underperform.

Even many individuals who invest in index funds get it wrong because they limit themselves to funds that mimic either the S&P 500 Index or a total U.S. market index. At the very least, they should also include a significant allocation (30 percent to 50 percent) to a fund such as Vanguard's Total International Stock Index Fund.

The next step is to show you how simple it is to build a more effective, globally diversified portfolio. Many investors think that diversification means owning enough mutual funds. However, the key is spreading them across asset classes. After all, 10 different large-cap growth funds still means you only have exposure to one asset class.

The Basic Portfolio

We will begin with a portfolio that has a conventional asset allocation of 60 percent stocks and 40 percent bonds. The time frame will be the 38-year period, 1975-2012. This period was chosen because it's the longest for which we have data on the indexes we need. While maintaining the same 60 percent stock/40 percent bond allocation, we'll then expand our investment universe to include other stock asset classes.

We begin with a portfolio that consists of just two investments:

- The S&P 500 Index for the stock allocation

- Five-year Treasury notes for the bond portion

We'll see how the portfolio performed if one had the patience to stay with this allocation from 1975 through 2011 and rebalanced annually. We will then demonstrate how the portfolio's performance could have been made more efficient by increasing its diversification across asset classes. We do so in four simple steps.

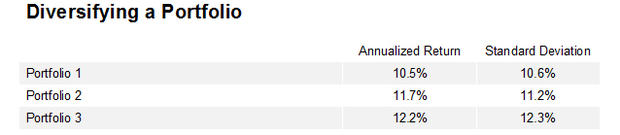

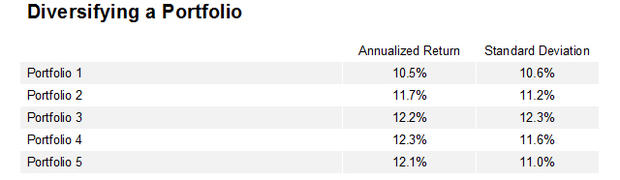

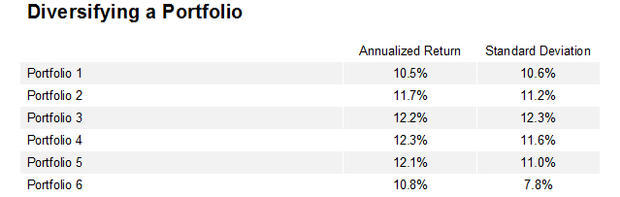

Portfolio 1

- 60 percent S&P 500 Index

- 40 percent five-year Treasury notes

By changing the composition of the control portfolio, we will see how we can improve the efficiency of our portfolio. To avoid being accused of data mining, we will alter our allocations by arbitrarily "cutting things in half."

Small-Cap Stocks

The first step is to diversify our stock holdings to include an allocation to U.S. small-cap stocks. Therefore, we reduce our allocation to the S&P 500 Index from 60 percent to 30 percent and allocate 30 percent to the Fama/French Small Cap Index. (The Fama-French indexes measure returns using the academic definitions of asset classes. Note that utilities have been excluded from the data.)

Portfolio 2

- 30 percent S&P 500 Index

- 30 percent Fama/French Small Cap Index

- 40 percent five-year Treasury notes

Value Stocks

Our next step is to diversify our domestic stock holdings to include value stocks. We shift half of our 30 percent allocation in the S&P 500 Index to a large-cap value index and half of our 30 percent allocation of small-cap stocks to a small-cap value index.

Portfolio 3

- 15 percent S&P 500 Index

- 15 percent Fama/French US Large Value Index (ex utilities)

- 15 percent Fama/French US Small Cap Index

- 15 percent Fama/French US Small Value Index (ex utilities)

- 40 percent five-year Treasury notes

International Stocks

Our next step is to shift half of our stock allocation to international stocks. For exposure to international value and international small-cap stocks we will add a 15 percent allocation to both the MSCI EAFE Value Index and the Dimensional International Small Cap Index.

Portfolio 4

- 7.5 percent S&P 500 Index

- 7.5 percent Fama/French US Large Value Index (ex utilities)

- 7.5 percent Fama/French US Small Cap Index

- 7.5 percent Fama/French US Small Value Index (ex utilities)

- 15 percent MSCI EAFE Value Index

- 15 percent Dimensional International Small Cap Index

- 40 percent five-year Treasury notes

The effect of the changes has been to increase the return on the portfolio from 10.5 percent to 12.3 percent -- an increase of 17 percent in relative terms. This outcome is what we should have expected to see as we added riskier small-cap and value stocks to our portfolio. Thus, we also need to consider how the risk of the portfolio was impacted by the changes. The standard deviation (a measure of volatility, or risk) of the portfolio increased from 10.6 percent to 11.6 percent -- an increase of 9 percent in relative terms. While returns increased 17 percent, volatility increased just 9 percent.

Commodities

There's one more asset class we want to consider including in a portfolio. As we discussed earlier, commodities diversify some of the risks of investing in stocks. They also diversify the risks of investing in bonds. Therefore, we'll add a 4 percent allocation to the Goldman Sachs Commodity Index, reducing each of our four domestic stock allocations by 0.5 percent and both the international stock allocations by 1 percent.

Portfolio 5

- 7 percent S&P 500 Index

- 7 percent Fama/French US Large Value Index (ex utilities)

- 7 percent Fama/French US Small Cap Index

- 7 percent Fama/French US Small Value Index (ex utilities)

- 14 percent Dimensional International Small Cap Index

- 14 percent MSCI EAFE Value Index

- 4 percent Goldman Sachs Commodity Index

- 40 percent Five-Year Treasury Notes

Most investors think of commodities as risky investments. However, you'll note that the addition of commodities to the portfolio actually reduced the volatility of the portfolio, and reduced it by three times the reduction in the portfolio's return. While the portfolio's return fell by 0.2 percent, its standard deviation fell by 0.6 percent. Relatively speaking, the portfolio's return fell 2 percent while its volatility fell by 5 percent. This "diversification benefit" is why you should consider including a small allocation to commodities in your portfolio.

The net result of all of our changes is that we increased the return of the portfolio by 1.6 percent, from 10.5 percent to 12.1 percent -- an increase of 15 percent in relative terms. At the same time, the volatility of the portfolio increased just 0.4 percent, a relative increase of 4 percent.

Reducing Risk

You have now seen the power of modern portfolio theory at work. You saw how you can add risky (and, therefore, higher expected returning) assets to a portfolio and increase the returns more than the risks were increased. That's the benefit of diversification. However, there's another way to consider using this knowledge. Instead of trying to increase returns without proportionally increasing risk, we can try to achieve the same return while lowering the risk of the portfolio. To try and achieve this goal, we increase the bond allocation to 60 percent from 40 percent and decrease the allocations to each of the stock asset classes and to commodities.

Portfolio 6

- 4.5 percent S&P 500 Index

- 4.5 percent Fama/French US Large Value Index (ex utilities)

- 4.5 percent Fama/French US Small Cap Index

- 4.5 percent Fama/French US Small Value Index (ex utilities)

- 9.5 percent Dimensional International Small Cap Index

- 9.5 percent MSCI EAFE Value Index

- 3 percent Goldman Sachs Commodity Index

- 60 percent Five-Year Treasury Notes

Compared with Portfolio 1, Portfolio 6 achieved a higher return with far less risk. Portfolio 6 provided a 0.3 percent higher return, 10.8 percent versus 10.5 percent -- a relative increase of 3 percent. It did so while experiencing 2.8 percent lower volatility, 7.8 percent versus 10.6 percent -- a relative decrease of 27 percent.

Through the step-by-step process described above, it becomes clear that one of the major criticisms of passive portfolio management -- that it produces average returns -- is wrong. There was nothing "average" about the returns of any of the portfolios. Certainly the returns were greater than those of the average investor with a similar stock allocation, be it individual or institutional.

Passive investing delivers market, not average, returns. And it does so in a relatively low-cost and tax-efficient manner. The average actively managed fund produces below market results, does so with great persistency, and does so in a tax-inefficient manner.

By playing the winner's game of accepting market returns, you'll almost certainly outperform the vast majority of both individual and institutional investors who choose to play the active game.

Money image courtesy of Flickr user Alex E. Proimos.