Get ready for the Fed's next scary policy change

The Federal Reserve is becoming increasingly aggressive with the monetary policy tightening campaign it started so hesitantly in December 2015, and the next phase of this campaign -- reversing its “quantitative easing” program -- could start soon.

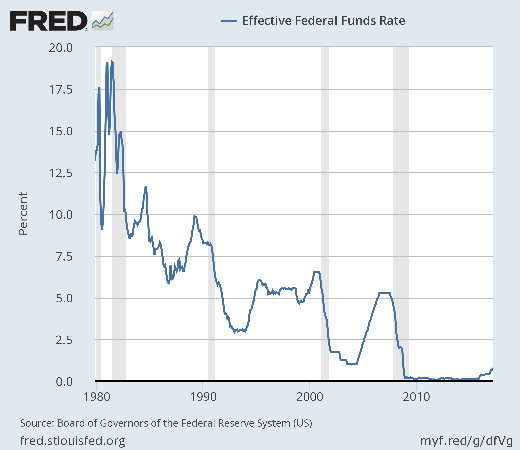

The Fed’s first move has been to raise its benchmark interest rates. After hiking rates just twice over 10 years, it has dramatically quickened the pace and did so again twice in the last three months. Wall Street analysts now expect two more increases this year -- in June and September -- pushing interest rates above the 1 percent threshold for the first time since the financial crisis (chart below).

It’s hard to overstate just how big a deal this all is: The U.S. is exiting the longest-ever period of cheap money stimulus and the largest-ever experiment in ultralow interest rates in human history. That’s not hyperbole.

As investors look ahead to the release of the latest Fed meeting minutes on Wednesday, all eyes will be on whether policymakers hint at a “balance sheet normalization” that will start the process of reversing the increase in the Fed’s asset holdings -- from $1 trillion before the recession to some $4.5 trillion now. Those assets were added via multiple purchase programs, including three rounds of quantitative easing (QE).

Trimming the Fed’s balance sheet, likely by allowing assets to “roll off” as they mature, will further boost interest rates because it will reduce the money supply available to capital markets. Policymakers have said in the past they would wait to have a conversation on this until interest rates rise well above zero.

That benchmark has now been reached.

Deutsche Bank economist Joseph LaVorgna warned that the Fed is in uncharted territory here. But it will nonetheless likely push ahead with balance-sheet tightening later this year or in early 2018 based on recent comments by New York Fed President William Dudley and others.

The risk is that markets overreact.

They sure did during the “taper tantrum” of 2013 when the Fed, under former Chair Ben Bernanke, hinted that it would begin reducing the rate of bond purchases under the “QE3” program, the third and final bond-buying binge. The 10-year Treasury yield surged from a low of around 1.6 percent to a high of more than 3 percent before settling back below 2.2 percent in 2014.

Current Fed Chair Janet Yellen will try to avoid this by “thoroughly preparing the markets” according to LaVorgna. That spadework could start with the release of today’s minutes from the March policy meeting.

Another wrinkle to the story comes from Oxford Economics, which noted that the Fed’s task is made more difficult by the uniqueness of this business cycle: Growth has been tepid as the scars of the financial crisis have often festered instead of healed. Job and wage growth has been underwhelming, for instance.

As a result, compared to past rate tightening campaigns, the Fed is starting this one very late in the cycle and from a very low interest rate base. It’s hard to exaggerate the risks of a policy mistake. And thus, Oxford has warned clients of the very real potential of a “severe market reaction” that could push interest rates dramatically higher and pressure equity and commodity valuations.

In other words, beware of an even larger version of the tantrum investors threw four years ago as the world they’ve grown comfortable in -- pampered by ultra-easy monetary policy and a dovish Fed -- is set to change in a big way.