For home insurance rates, it's location, location, location

If you're thinking of buying a waterfront home in Florida, think again. Homeowners' insurance rates in the Sunshine State could send you packing faster than the next hurricane.

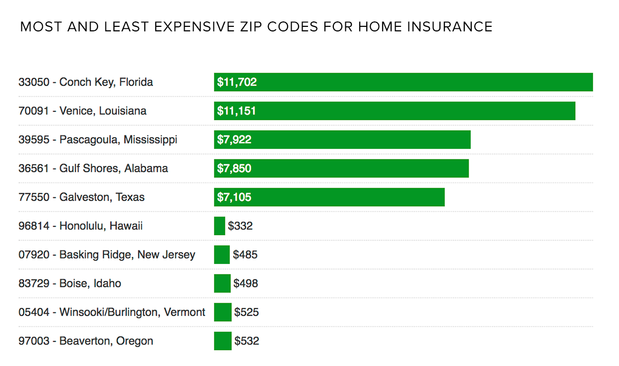

Insurance for a house on Conch Key -- one of the state's string of islands separating the Atlantic Ocean from the Gulf of Mexico -- would cost you an average annual premium of $11,702, according to a survey of all the nation's zip codes done by online website Insurance.com.

If that's a surprise, it shouldn't be. Conch Key was battered last month by Hurricane Irma as it stormed through Florida with 135 mile-per-hour winds. The real surprise would be if rates there don't go up even more. The same holds true for other coastal states with frequently flooded areas such as Venice, Louisiana; Pascagoula, Mississippi; and even the golfer's paradise of Myrtle Beach, South Carolina.

And places like Garden City, Kansas, and Forest Park, Oklahoma, which both lie in tornado alley, are also unable to escape insurers' radar.

But what about Honolulu, where 1992's Hurricane Iniki is still vividly remembered. The average yearly premium there is only $332. What's so special about the Aloha State? It doesn't allow homeowners' credit scores to be used in deciding how much is paid, and its homeowners pay a separate premium for hurricane insurance.

While the Insurance.com survey isn't a perfect representation of the cost differential for homeowners' insurance, it comes very close. It breaks down the price for insurance by zip code and amount of money needed to pay that yearly bill at 75 different coverage levels, depending on dwelling size, deductible and liability coverage -- if, for example, someone slips and falls on the property.

The survey sampled six insurers in most states.

But its results are likely to leave consumer advocates enraged. Some of the poorest areas pay the most, while wealthier areas pay a lot less for the same basic insurance coverage. In New Jersey, residents of down-on-its-luck Atlantic City pay more than those living in Basking Ridge, a wealthy community outside New York City.

That's the way the industry works. Home insurance varies by location, which reflects not only storm damage, but wild fires and burglaries, so police presence and fire stations factor in. Credit score, marital status and age are also important. Insurers also take into account whether you've filed a previous claim.

Since insurers don't like paying claims, collecting on one can target not only you, but your house as well. "Even if you didn't file a claim on your house and the previous owner did, the insurer will still label the home as a higher risk," said Michelle Megna, an editor at Insurance.com.

Even worse: Your neighborhood's claims history could count against you. And the closer you are to your neighbors, the more you may have to pay. "Cities with low population densities will have lower insurance rates," said spokesperson Michael Barry of the Insurance Information Institute, which represents property-casualty insurers.

In retrospect, everything is going against Conch Key. Not only Hurricane Irma but high home-repair costs because contractors have to travel a long way to get to this outer island.

On top of that, contractors have targeted Florida with what Insurance.com sees as a "scam," whereby they get waterlogged homeowners to sign an "Assignment of Benefits" form that gives the contractor the right to submit "inflated claims" to the homeowners' insurance company.

The insurer's response: a rate increase for the homeowner.