Why federal debt may have to explode before it shrinks

On Tuesday night, President Donald Trump will address a joint session of Congress for the first time. For a country still suffering from bitter political divisions after a contentious election, it’s doubtful his speech will heal still-raw emotions. Especially since Mr. Trump has hinted that he’ll discuss his budget plan, including a big statement on infrastructure spending and sharp cuts to federal agencies.

No matter what you think of President Trump -- whether you see him as a buffoon, a wannabe despot or the savior who’ll finally Make America Great Again -- here’s one big reason you should have some sympathy for him: He faces the worst fiscal outlook of any recent president.

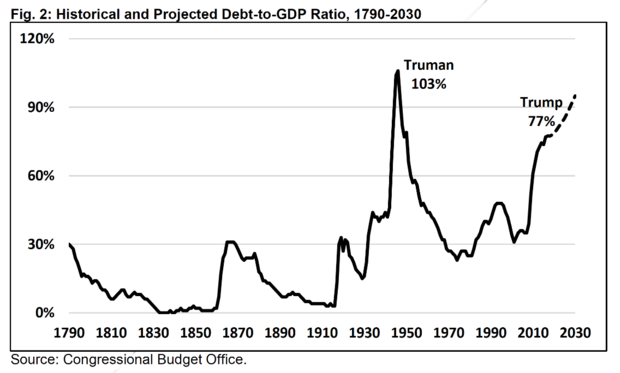

He has taken office with the national debt nearing $20 trillion and debt held by the public above $14 trillion. According to the Committee for a Responsible Federal Budget (CRFB), debt is at a higher levels as a share of the economy than for any incoming president since Harry Truman in 1945 (chart below). Yet unlike Truman, who was handed an economy demobilizing from the fight against the Japan and Nazi Germany, the national debt is expected to continue to rise during Trump’s presidency and beyond.

Moreover, federal spending on entitlements and interest payments represents a larger share of the budget than under any other president, leaving Mr. Trump with far less room on the “discretionary” side of the budget. Adding a sense of urgency to all of this, three federal trust funds -- covering highways, Social Security Disability and Medicare Hospital Insurance -- are headed for insolvency over the next eight years, with a fourth set for depletion in 2030 (Social Security Old-Age Trust).

That complicates the tax reform effort the president championed on the campaign trail and touted again recently, saying his tax plan would be something “phenomenal,” with details to come within weeks. What we already know: Mr. Trump and Republicans in Congress want a simplification of the tax code and a cut in overall tax rates for households and corporations.

A tax cut will surely worsen the deficit over the near term. Yet it could also be necessary for invigorating the economy and quickening the growth needed to fix the long-term fiscal outlook. However, the efficacy of a tax cut providing fiscal stimulus is a matter of intense debate, to put it lightly, with economists evenly split on the subject according to a recent survey.

For Mr. Trump, perhaps the only way out of this fiscal bind is by worsening it temporarily, mixing a well-designed tax reduction and reform plan with targeted spending cuts and entitlement reform. No easy task. But a survey of the literature, including this 2014 paper from the Brookings Institution, suggests benefits can result from simplifying the tax code, lowering rates, and cutting “unproductive” federal spending.

According to Deutsche Bank economist Joseph LaVorgna, although the current economic expansion has been feeble and is now in its eighth year, there “remains considerable room for cyclical gains in consumption.”

With the unemployment rate below 5 percent, LaVorgna doesn’t believe job growth alone can do the trick. But a combination of personal tax cuts and wage inflation -- driven by corporate tax reforms like full expensing that encourages capital spending and labor productivity gains -- could do it.

LaVorgna is more optimistic than others, including the CRFB, which warns that the economy can’t sustain the 3.5 percent annual GDP growth Mr. Trump needs to pay for his tax plan and bring the deficit down.

The debate will surely flare up anew on Wednesday morning following the president’s speech. And with the statutory federal debt limit approaching sometime in March, the need to do something about the fiscal mess will grow increasingly acute very quickly.