Morningstar Expert: Investing Help for Your 401(k)

In her new book, 30-Minute Money Solutions: A Step-by-Step Guide to Managing Your Finances, Morningstar Director of Personal Finance Christine Benz offers a simple three-step plan for investing your 401(k) plan. Benz says you first need to decide how much control you want over your retirement portfolio.

For most 401(k) investors, the best strategy for managing a retirement portfolio falls somewhere in between the do-nothing approach and being a hyperactive trader. To take the middle course and select the best investments in your company retirement plan, you’ll need:

- A menu of the choices available in your 401(k) plan

- A rough idea of when you expect to retire

- The appropriate stock/bond mix for you given the number of years you have until retirement

3 Ways to Invest

To spend very little time creating and maintaining your retirement plan, see if your company offers a target-date fund with a stock/bond mix appropriate for someone your age that gradually becomes more conservative as you get closer to retirement.

As good as the target-date fund concept is, not every fund company has executed it well. Some are too costly: An expense ratio higher than 1 percent a year is a red flag. Also, the funds may have stock/bond mixes that are too aggressive or too conservative. To see how your plan’s funds score, go to Morningstar.com, type in the target-date fund to find its Asset Allocation breakdown, and compare it with the pie chart for your target date. If the fund diverges widely from the chart, investigate further before using it as the linchpin of your company retirement plan.

To take more control over your 401(k) or if your plan’s target-date funds aren’t very good, use low-cost index funds. To build an all-index-fund 401(k) plan, choose your asset allocation and direct the appropriate percentage of your contributions to the corresponding index funds. Say you plan to retire in 2040. You could put 50 percent in a total U.S. stock index fund, 25 percent in a total foreign stock index fund and the rest in a total U.S bond index fund. You’d need to make changes to your portfolio only when your asset allocations get out of whack with your targets and by making your portfolio more conservative as you near retirement.

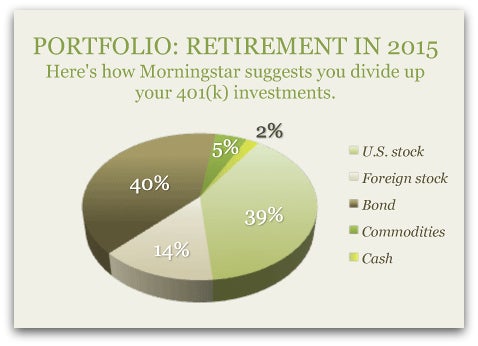

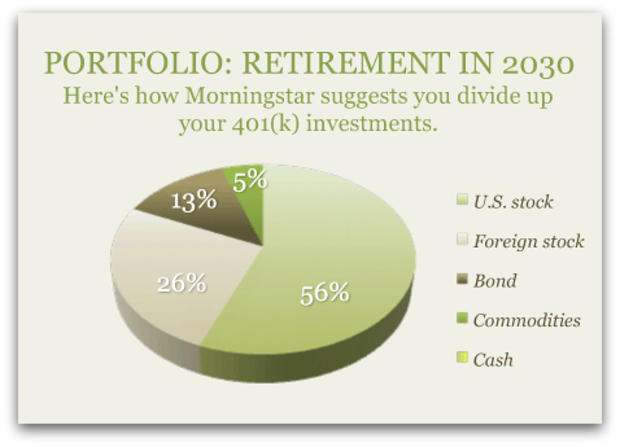

These pie charts show Morningstar’s suggested Lifetime Allocation Indexes. For example, someone hoping to retire in five years would want a portfolio with more than 40 percent of the money in bond funds.

Meanwhile, someone who won’t retire till 2030 should have only 13 percent in bonds, and more than 80 percent in equity funds.

To try to beat the market, you can use index funds for the core of your portfolio and actively managed funds to supplement them. This will mean investing more time at the outset than using just index funds, spending time identifying worthy managers, and conducting ongoing oversight to ensure they’re meeting your expectations and are still at the helm.

When selecting active funds, you might be tempted to invest in the ones with the best returns over the past several years or to focus on those with 4- or 5-star Morningstar ratings. Don’t just stop there. Look to be sure that the manager has had at least a five-year tenure. You’ll also want to gravitate toward the lowest-cost options in your plan. Look for stock funds with expense ratios of less than 1.25 percent, and preferably much lower than that. You’ll want bond funds costing less than 0.75 percent.

Successful investing doesn’t require complex strategies. If you can get the big-picture decisions right, you’ll be well on your way to financial success.

From 30-Minute Money Solutions: A Step-by-Step Guide to Managing Your Finances by Christine Benz. Copyright 2010 by Morningstar Inc. Reprinted by permission of John Wiley & Sons, Inc.

More on MoneyWatch: